Over the last 18 months we have seen unprecedented highs and huge fluctuations in energy prices, sometimes all within the same trading session. A little over 12 months ago forward annual gas prices were at 334p/therm, the same annual contract now trades at 125p/therm.

While some people are accepting this as the new normal, the energy market remains in a precarious place, with several factors having the potential to drive prices up quickly. The nature of these factors means that now, more than ever, it is vital for all organisations to act decisively to implement the correct procurement strategy to mitigate the risk these factors present.

We have outlined the factors below, highlighting how they could impact the price of energy over the coming months.

The difference between a mild and cold winter.

It goes without saying that the best case scenario for the UK is that we have a mild winter. If this happens then prices are likely to remain weak. However, if we have an extended period of cold weather this may well push prices higher. In December 2022, when temperatures were below average, day ahead prices averaged 268p/therm on gas and £241/MWh on electricity. These prices are significantly higher than the current forward curve.

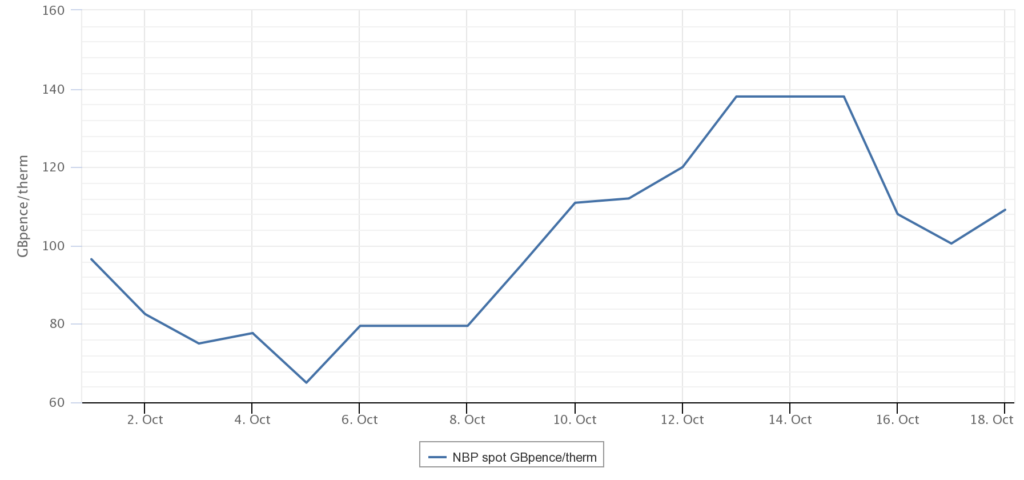

October 2023 is a great example of the weather’s impact on energy prices. The first week was warm, the second week was cold. The below chart shows how an extremely mild start to October pushed day ahead prices to less than 80p/therm but during the colder period in the middle of October we saw spot prices of almost 140p/therm.

One positive right now is that EU gas storage inventories are very high, but a sustained or early cold period could dwindle those stocks quickly.

The impact of supply and demand.

The impact supply and demand has on energy prices cannot be understated. Since the Ukraine conflict began, we have removed our dependency on Russian gas. However, more than ever we are now at the mercy of global gas prices and the activity of countries such as China and India.

While gas demand from countries such as China has been subdued recently, if that demand returns quickly the impact will be felt across the world. It may drive up energy prices in the UK and across Western Europe.

A cold winter in the UK and an increase in demand for Liquid Natural Gas (LNG) from China and India could drive up energy prices in the UK as supply constricts. However, the reverse is also true, a warm winter and stable demand for gas may see prices remain stable.

Global instability and energy security.

Just as the Ukraine conflict created volatility in the energy markets in 2022, the growing instability in the Middle East is increasing concerns about short-term energy security. Since the Hamas attack on Israel, Asian spot prices for LNG rallied about 25% as fears grow around global energy security.

It is not just gas prices that increased, crude oil prices rose as markets worried about the potential disruption to global oil supplies. Prices have since decreased since the Israel conflict began but if the conflict was to escalate further and other Middle Eastern countries were to be drawn into the situation, this would only create more uncertainty and therefore price volatility.

One country that is being monitored closely is Qatar, as it is a significant LNG supplier to Western Europe. Any issues around supply or shipping logistics through the Suez Canal, are likely to push energy prices higher.

While the influence of Russian gas has been widely negated, Western Europe continues to be supplied by Russia through both a pipeline transiting Ukraine and LNG coming into Belgium. If events in the Ukraine conflict were to deteriorate further this could lead to this supply ceasing and energy prices increasing.

The sabotage of key energy infrastructure.

Two years ago, this wouldn’t have been a consideration, however, we now know how vulnerable our utility infrastructure is. Over the last twelve months, there have been the Nordstream 1 gas pipeline explosions, the Finnish/Estonian pipeline leak caused by suspected sabotage (at the time), and the damage to the Sweden-Estonia telecom cable.

The probability of sabotage to a major pipeline remains low but the consequences could be catastrophic for energy prices.

We have subsequently learnt that the Finnish/Estonian pipeline leak may have been caused by a rogue anchor but it does highlight the vulnerability of our energy infrastructure.

So why is now the time to act?

The four factors we have outlined present risks, both on the upside and the downside, however, we would advise all organisations to consider their current and future exposure right now. There is a cost to being decisive as wholesale energy markets retain risk premiums at the present time however, by planning now, your organisation will have greater certainty on energy costs and the financial impact on your business operation.

The same can’t be said for the financial impact should we encounter a cold winter and increased instability in the Middle East. Our advice is that you shouldn’t wait and attempt to buy at the perceived bottom of the market, as no-one knows when that bottom is. You should implement the appropriate risk management strategy, whether that is through a fixed energy contract, entering a flexible procurement basket, or with a standalone flexible procurement strategy.

Reach out to our team on 020 3813 1550 or email us at [email protected] so we can help you explore your energy procurement options.

Get in touch

Author – Alastair Hutson

Article published 16.11.2023

All prices correct at time of publication.